Electric Capital's 2024 Developer Report

Seven insights from the 2024 Developer Report

Developer activity is one of the most fundamental metrics for evaluating the future of blockchain or digital asset projects. More developer activity means more potential for growth, more access points, and more apps and services.

Slowing or dwindling developer interest might indicate that a project is losing steam or that adoption is waning.

Interestingly, as valuable a metric as developer activity is, it is also the most under-reported, and it needs more visibility compared to other kinds of digital asset data.

One of the main reasons is that financial metrics, like market cap or TVL, are usually the brightest lights in the room when looking at onchain activity or growth. In many cases, financial metrics are valuable and popular because they are easy to understand and obtain.

The issue is that financial metrics can also be fuzzy or easy to game or manipulate. Countless examples of inflated token prices or other economic data don't match reality or utility.

Developer metrics might be less glamorous than rocketing prices. However, understanding which chains developers are working on is a good way for market watchers to know where things are headed.

That's why the annual Developer Report from Electric Capital is so valuable.

The report aggregates data from across the onchain space and worldwide and combines it to help give market moves and narrative trends more context.

To see how this year's trends and analysis compare to last year's report, check out this post:

Seven insights from the 2024 Developer Report

Before diving into the takeaways from this year's report, it's important to note that the data that makes the basis for the report was collected based on code commits made in GitHub, a popular code repository for open-source projects.

In other words, this report's existence is a great example of why building with transparent systems is such an important component of Open Money.

With that out of the way, here are the trends:

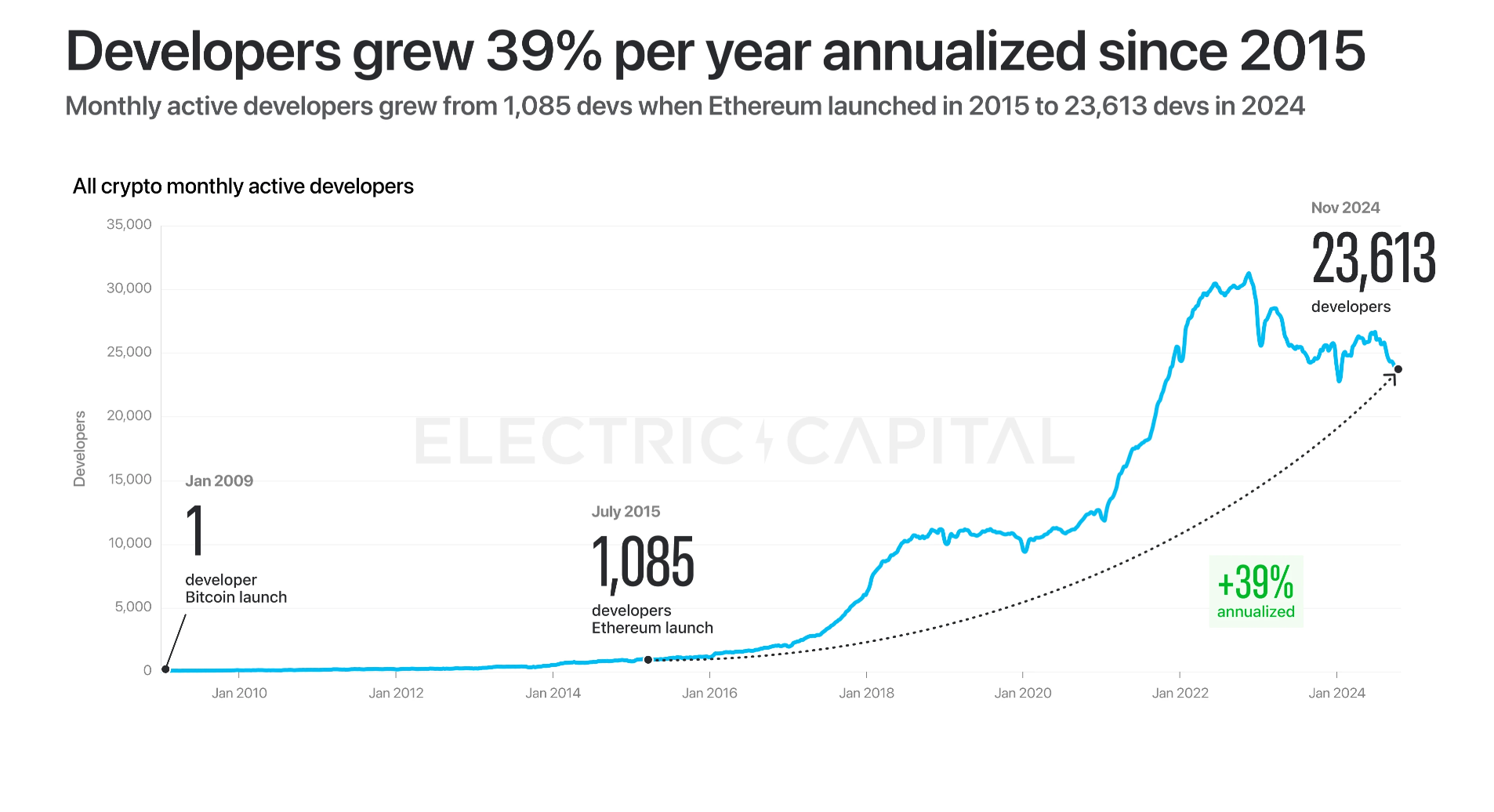

Crypto developer activity continues to grow

Crypto bull markets attract a new crop of developers. And while there is always a dropoff in developer activity during bear market cycles, the number of experienced developers (with 2+ years of experience) continues to grow.

The number of experienced developers grew by 27% in 2024. This growth matters because 70% of code commits come from this group of more experienced developers.

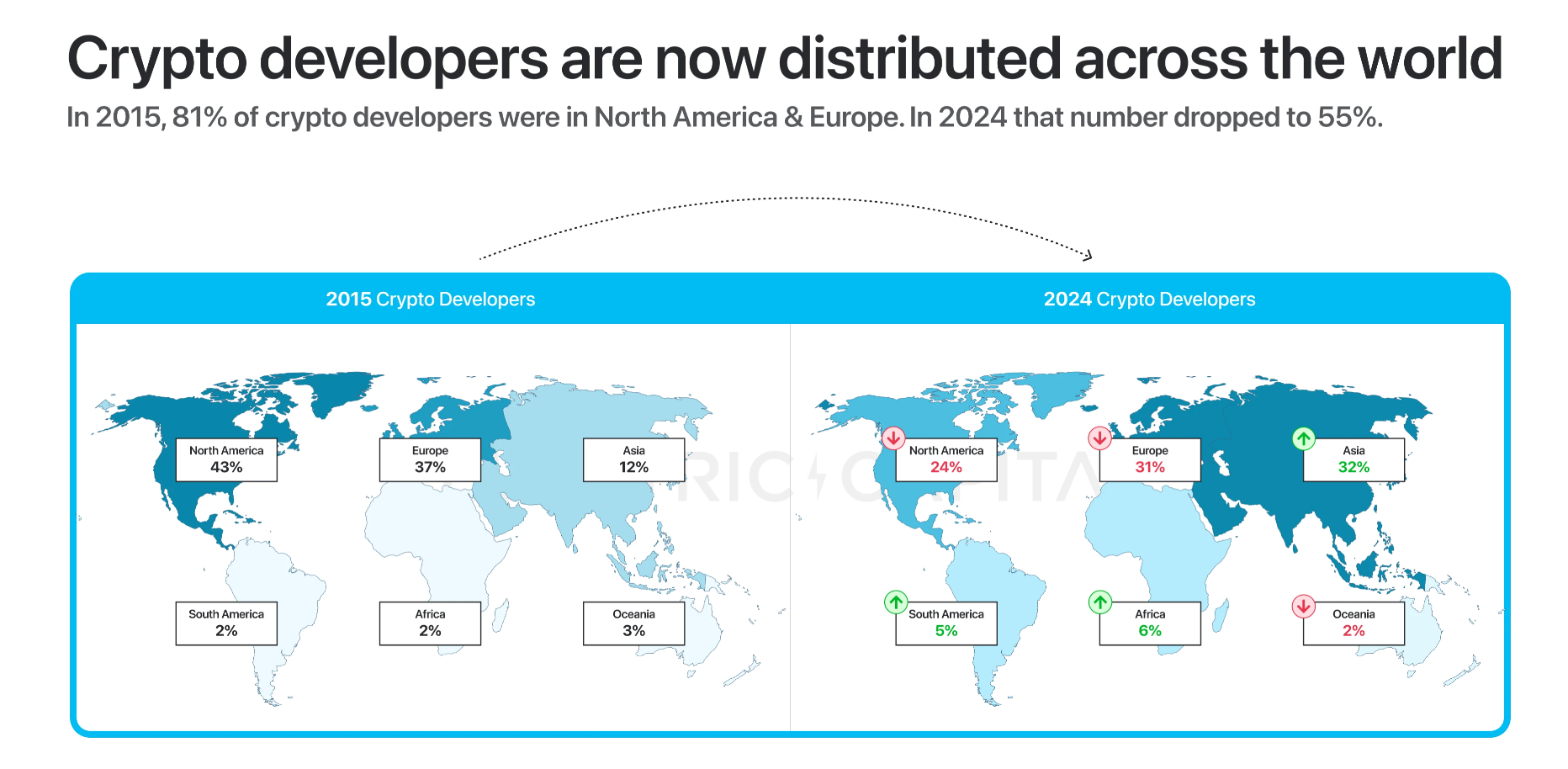

Developer activity is becoming more distributed around the world

North America and Europe are losing developers. Now, 1 in 3 developers live in Asia.

India is the source of the most new developers, pulling past the United States in 2023.

Africa and South America are also gaining developers, with Africa outpacing South America for the past few years.

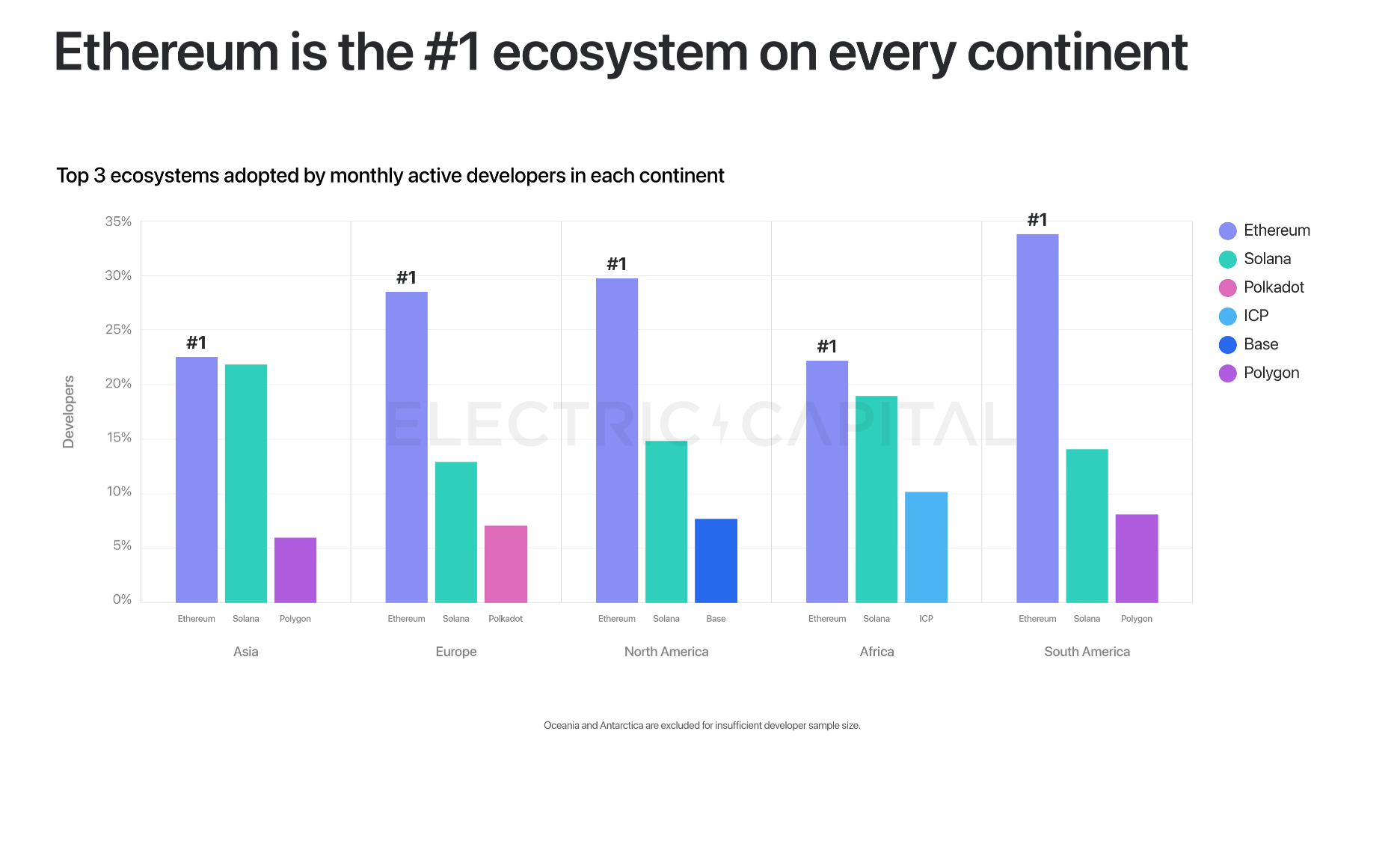

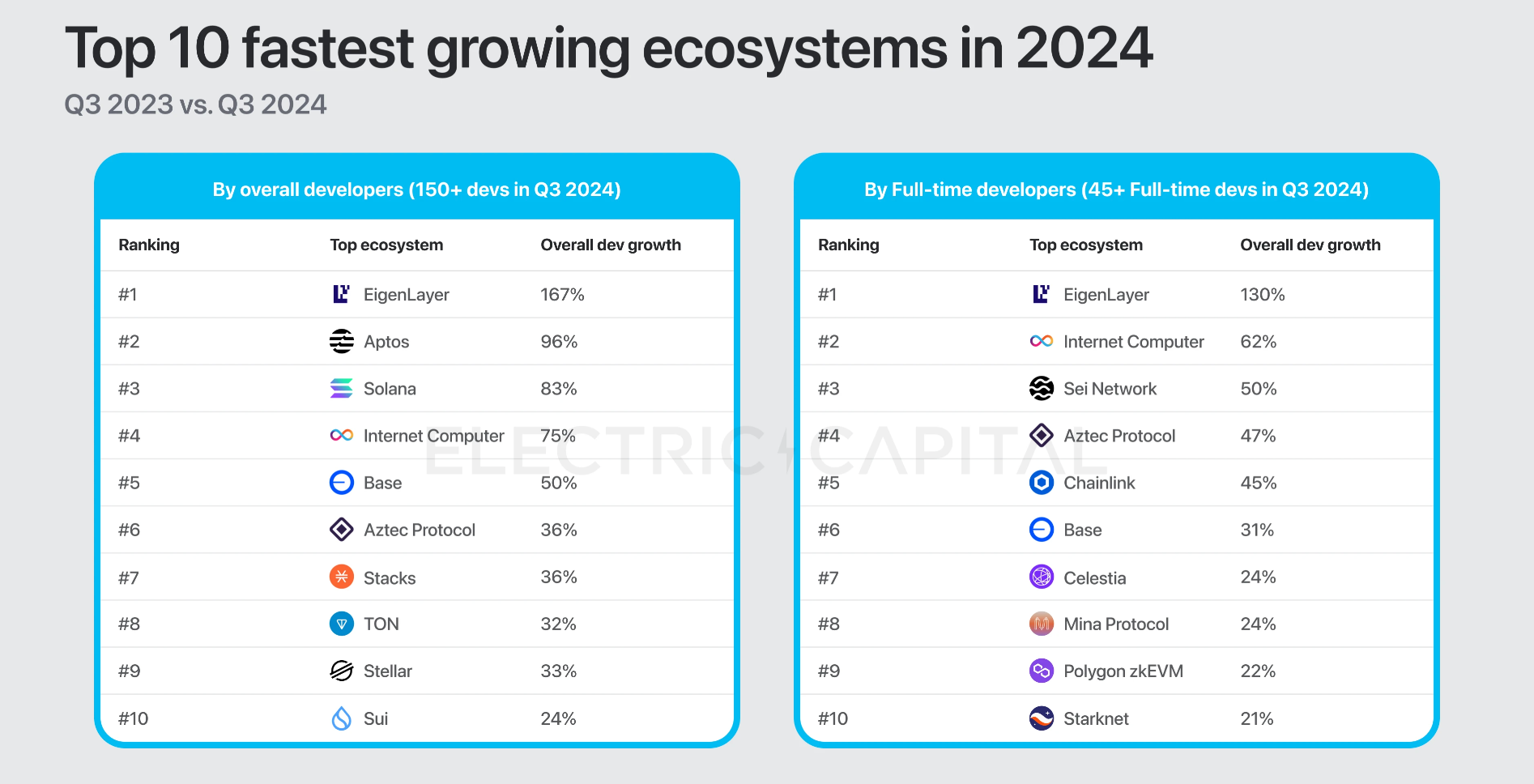

Developer activity: Ethereum and Solana are the two most popular developer platforms -- Bitcoin developers working on scaling

What's interesting about this data is that while Ethereum continues to be the most popular platform for established developers, Solana is more popular for new developers.

It's also interesting that it's not clear platform-wise what comes after second place for developer activity. Base, Polygon, Polkadot, and ICP are all in contention for the third-most-popular chain.

Blockchain developers are increasingly working on more than one chain, with 1 in 3 working on more than one chain.

Overall, the level of Bitcoin developer activity has remained consistent with last year in terms of volume. What's noteworthy is that 42% of Bitcoin developers are working on scaling solutions.

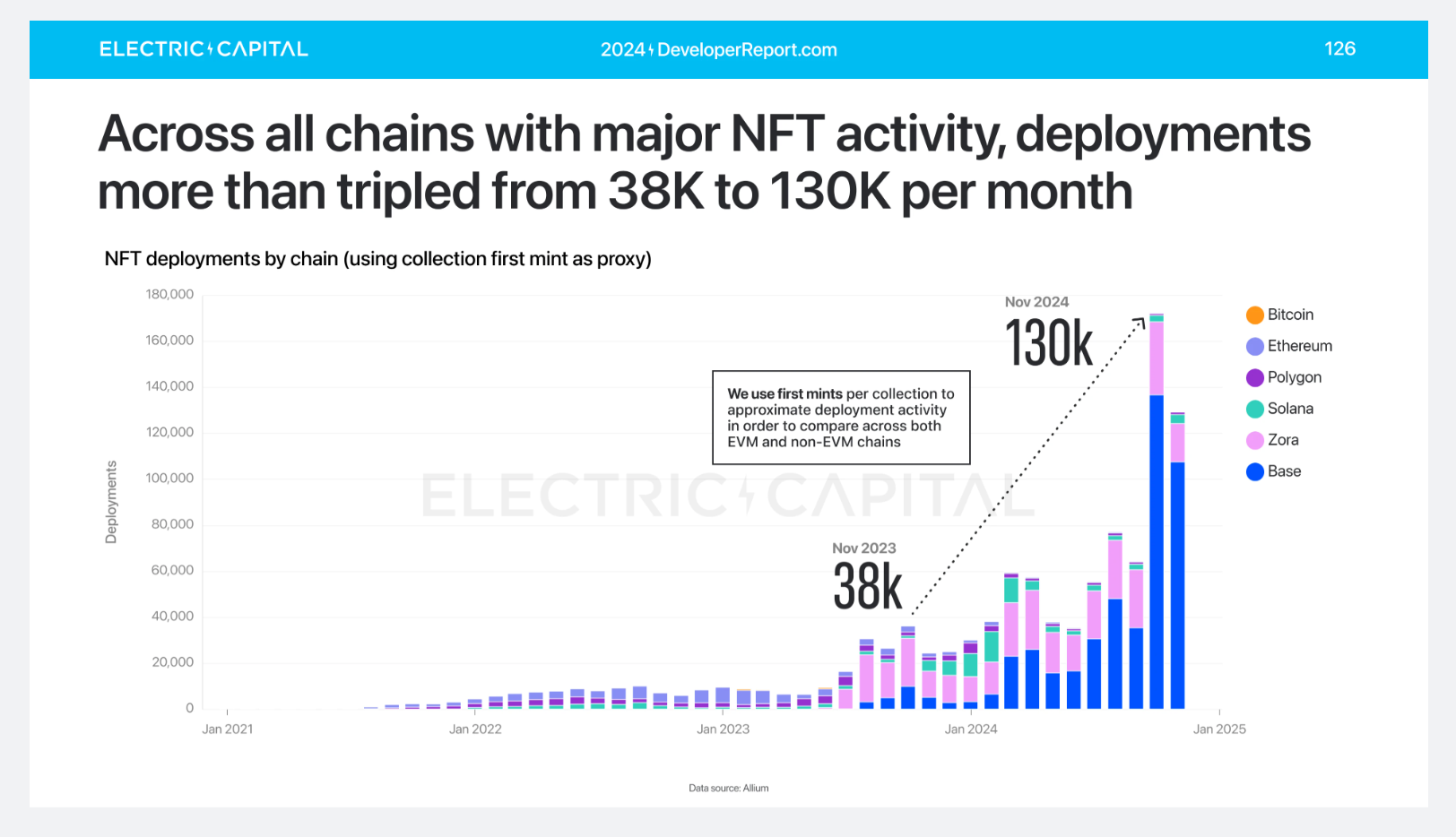

Onchain activity: Minting NFTs

Are NFTs back? In 2024, the number of wallets with minting activity hit 67 million, with the most minting activity on Solana, Polygon, and Base.

Minting transactions grew from 153 million in 2023 to 568 million in 2024.

While market watchers tie previous spikes in NFT activities to digital art and collectibles, the 2024 non-fungible token mint rally was more distributed among NFT use cases and included DeFi utilities, rewards programs, identity applications, and gaming.

February saw the most significant spike in minting-related activities.

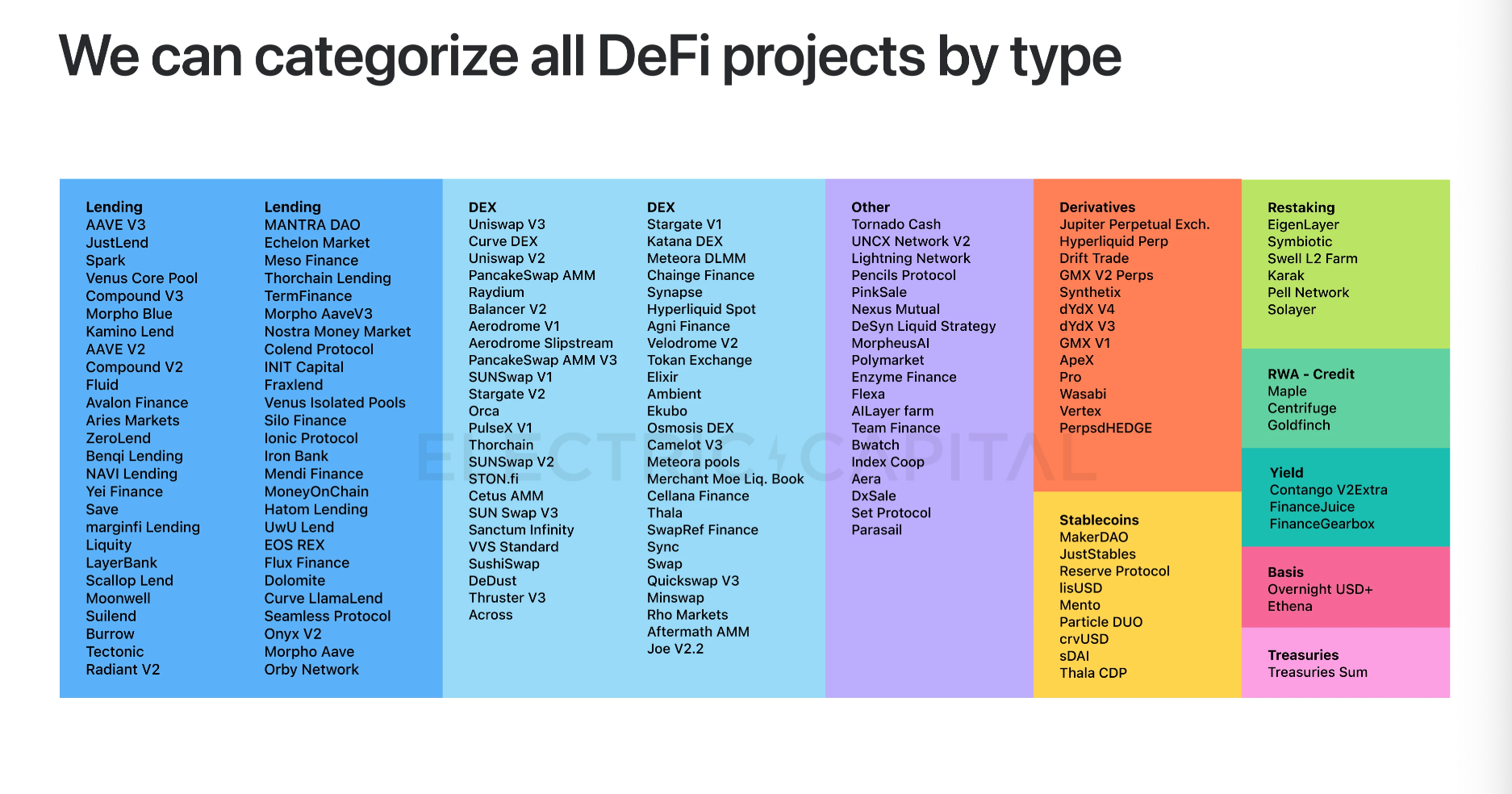

DeFi

Innovations continue to hit the DeFi market, with Ethereum still the clear winner for onchain DeFi providers. For more context, Ethereum DeFi is seven times larger than the next biggest chain, Solana.

Market charts reflected EigenLayer's continued growth. Restaking is now the largest sector within DeFi, accounting for $30.6B TVL, representing 1,818.47% year-to-date growth.

Solana is a leader in the decentralized exchange (DEX) use case. In 2024, 81% of all onchain DEX volume happened on Solana.

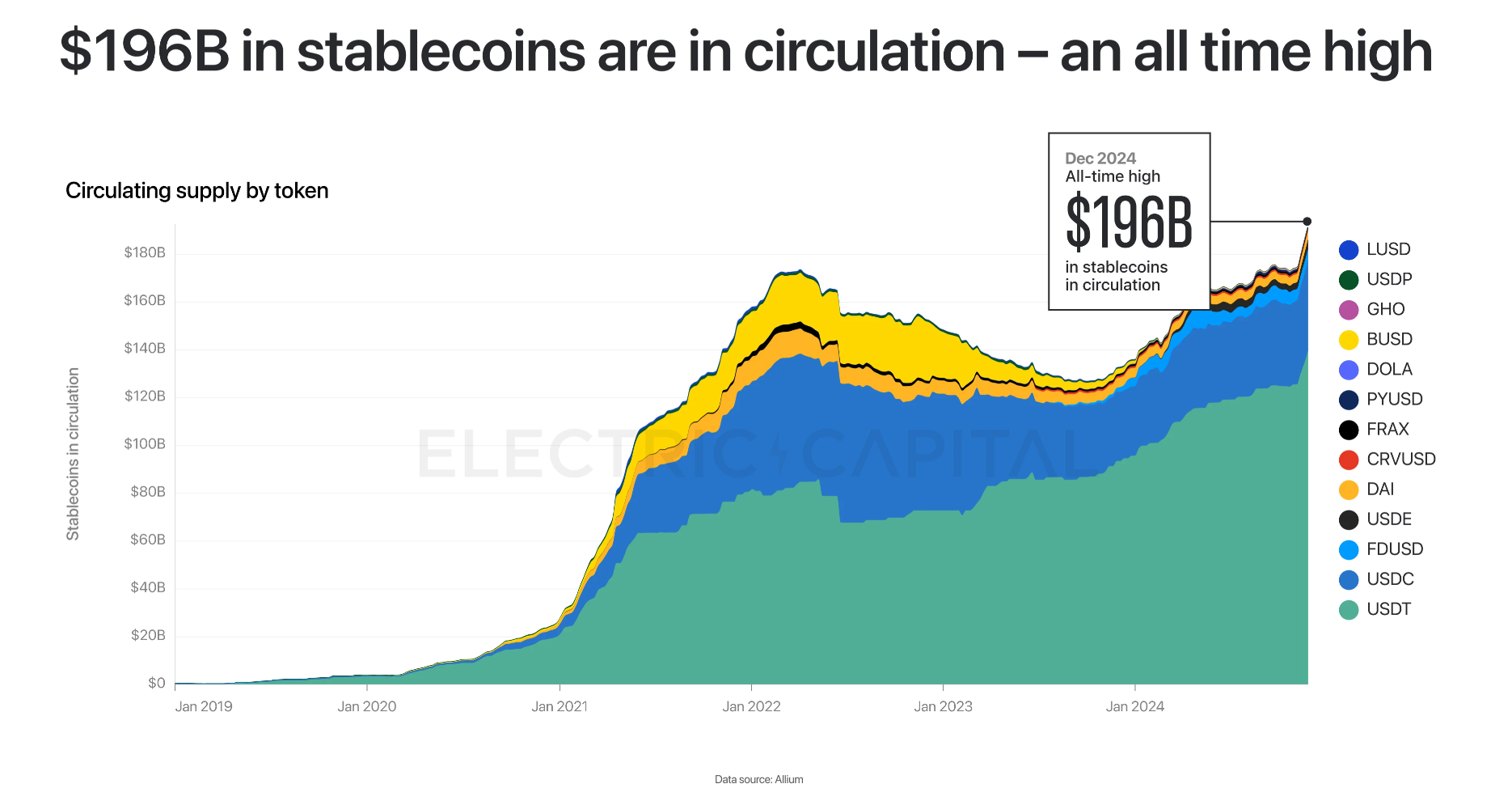

Stablecoins

A big trend for 2024 was the rise in the use and utility of stablecoins as a valuable digital asset.

Stablecoins broke all kinds of records in 2024. There are now $196 billion in stablecoins in circulation, and $81 billion in stablecoin volume is transacted every day.

Ethereum is still the dominant stablecoin platform, with 59% of all stablecoin transactions happening within the Ethereum ecosystem.

A trend within the larger stablecoin adoption story is using stablecoins to back real-world assets, such as US Treasuries, which do not account for $90 billion on stablecoins.

What does developer activity say about what to expect in 2025?

One of the most striking aspects of the 2024 Developer Report was how the major developer trends seemed to be in sync with the major narrative trends of the year.

For example:

- The surging popularity of stablecoins

- The adoption of Base as an easy-to-use platform for builders. (Here's a database of Base projects).

- Solana is a growing platform for NFT projects and a popular memecoin launcher.

Overall, developer activity is growing at a steady pace (despite regular market fluctuations). The continual distribution of developer talent around the world is another example.

Here's where you can find the complete report: